Anand Sanwal, founder of the New York-based venture database company CB Insights, made an unpleasant discovery yesterday after his subscribers pointed him to a TechCrunch piece about Techlist, a new venture database business.

Anand Sanwal, founder of the New York-based venture database company CB Insights, made an unpleasant discovery yesterday after his subscribers pointed him to a TechCrunch piece about Techlist, a new venture database business.

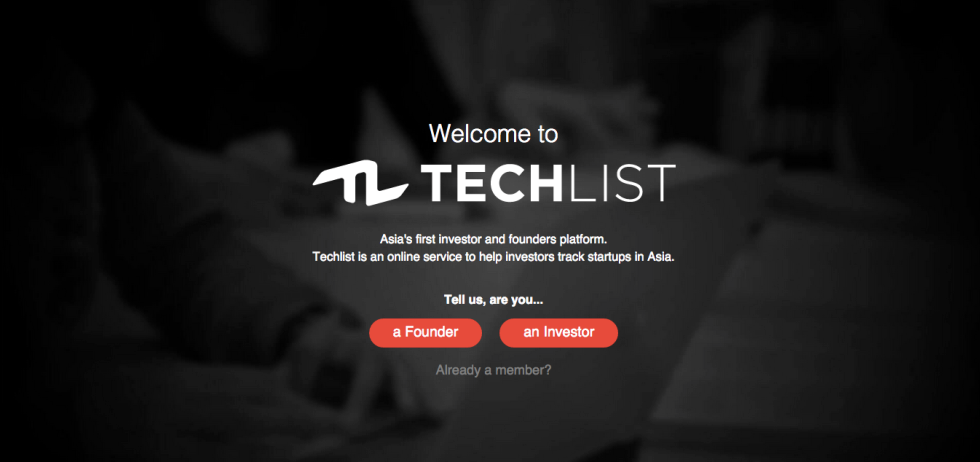

Techlist made the news because the outfit — a subsidiary of the Singapore-based media company Tech In Asia — was just admitted to the winter class of the prestigious accelerator program Y Combinator. The problem spied by Sanwal and his customers: Techlist has borrowed heavily from CB Insights’s design and user interface. The company clearly “crossed over from inspiration into plagiarism,” says Sanwal.

Whether Y Combinator agrees remains to be seen. But Sanwal – whose bootstrapped, 27-person company is competing against a growing number of new investor database companies — isn’t imagining things, seemingly. In recent months, 12 Techlist employees have seized on a 30-day trial period that CB Insights offers, including Tech In Asia’s CEO, Willis Wee, his head of product, and numerous product managers and developers.

Indeed, on Twitter yesterday, Wee acknowledged using CB Insights “as a reference to launch fast,” writing to Sanwal specifically, “Credits to you and we will be improving as we go along.”

Wee — whose company has previously raised venture funding from East Ventures and Simile Venture Partners — quickly added that Techlist is “very very different from any other venture database out there.”

StrictlyVC chatted with Sanwal yesterday about what happens next.

You just wrote a jokey post about “arriving” now that you have a “copycat.” Are you thinking of taking further action?

We’ve talked to our lawyers and are awaiting their guidance. Since Willis admitted on [Hacker News] and via Twitter [that] they copied, a lot of the gray area has been removed. But ultimately, this is a distraction, so [I’m] not sure what we’ll do. Plus, I love our lawyers, but they ain’t cheap.

Techlist plans to zero in on the Asian market. How big an area of focus is that for you?

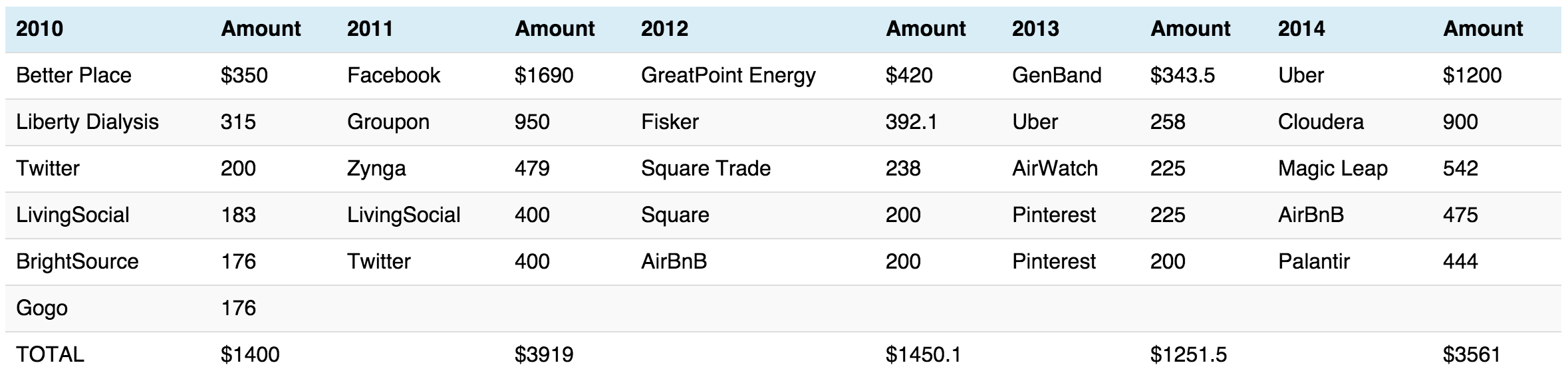

We cover financing and exit data globally, including Asia, as our institutional clients expect that we’re comprehensive. Also, Asia is our second fastest-growing market in terms of clients, so we’re putting a lot of effort on the area.

Have you asked Y Combinator for comment?

We haven’t. For the record, we don’t think this is YC’s fault. They have a lot of companies and cannot audit the UI/UX of their portfolio companies. I also don’t think [President] Sam [Altman] and the team condone this type of thing or think great companies are built by copying other companies. That said, I am curious to see what YC does.

Just yesterday, the WSJ published a piece about the advantages that venture-backed companies have over those that choose to bootstrap, including investor connections. How big a concern is this company and its investor ties?

It’s annoying, mainly because our team works hard, and I feel this is sort of crappy for them. But beyond that, we’re not concerned. Money buys you time, not the ability to execute. And we’ve seen lots of well-funded companies come into our space and all flame out.

You seem to be maintaining a sense of humor about this.

We’re a heads-down, low-drama group, so this made things interesting for us today. I realized that some drama from time to time is fun.

Sign up for our morning missive, StrictlyVC, featuring all the venture-related news you need to start you day.